We are excited to share with you all our latest long term investment position, Toast.

How We Found It:

Our interest in Toast started organically from two visits to restaurants over Thanksgiving. We noticed servers using a sleek handheld device to take orders and process payments tableside. We could tap to pay and leave immediately, with no waiting for the check. It was a meaningfully better experience.

The second time we saw the same device, we made a point of writing down the name, Toast. We then went back to the first restaurant to confirm, and sure enough, they were using it too.

From that point on, every restaurant and coffee shop we visited, we made sure to check what their ordering and payment systems were. The results were consistent, the majority of the locations we visited were running on Toast. When we traveled home for Christmas and repeated the exercise, 8 out of 10 places we visited for food or coffee were using Toast.

At this point, we wanted qualitative validation, not just our own observations, but feedback from the people actually using the software day to day. We began speaking with servers and managers at the locations we visited. The feedback was remarkably consistent. Not a single person had a negative word about the software itself. The only friction mentioned was the operational lift of switching from paper to digital, and even then, multiple people noted that Toast’s onboarding team was hands on throughout the transition, helping with training and setup.

Across all of our conversations, four themes emerged consistently:

Faster order entry

Fewer mistakes

Ability to serve more tables

Improved kitchen efficiency

Based on our interactions with restaurant workers, we felt that there was something worth researching.

About the Company:

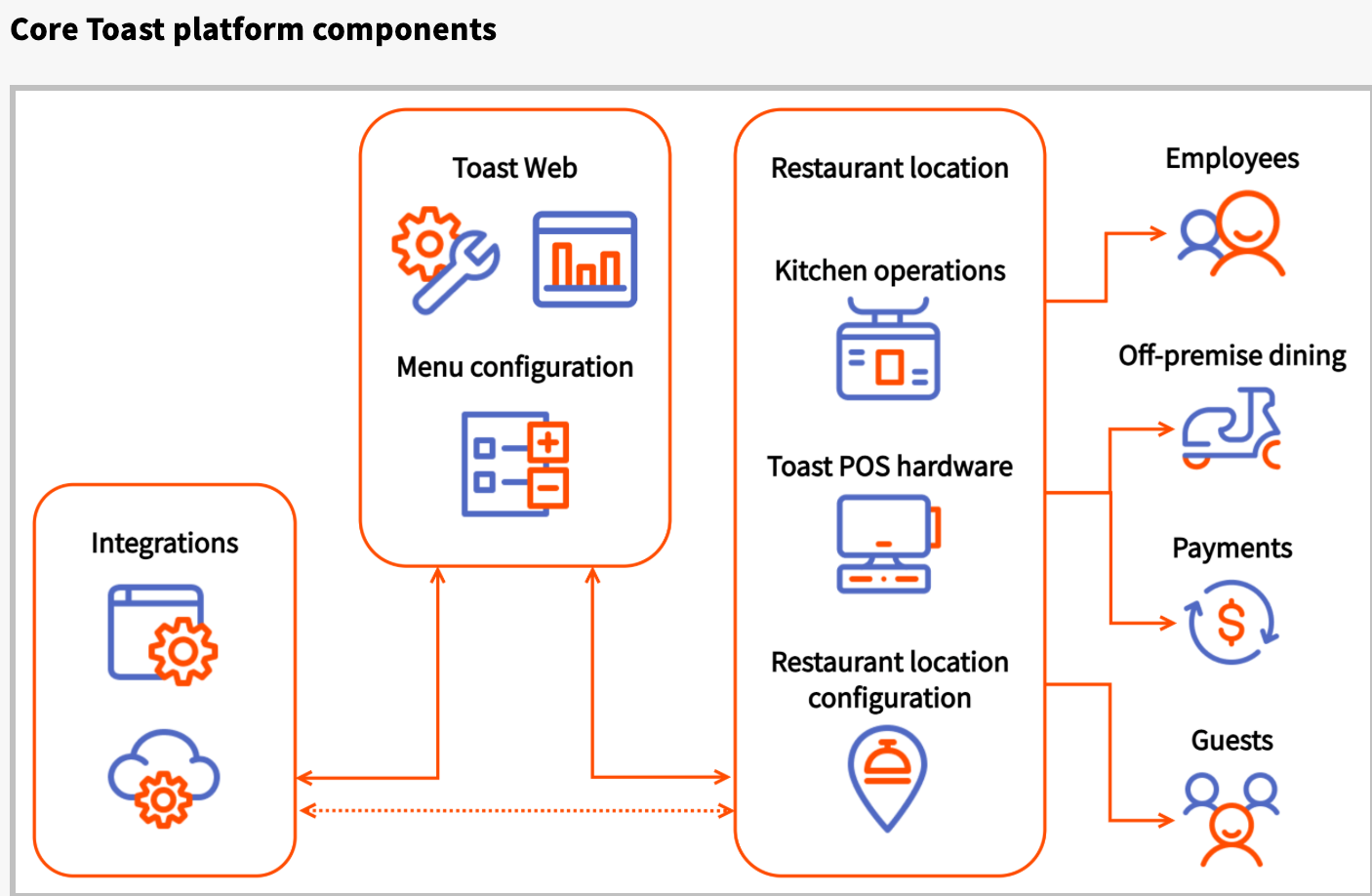

Toast is a cloud based, all in one technology platform purpose built for the restaurant industry. Through a single unified system, restaurants can manage point of sale, payments, digital ordering and delivery, marketing and loyalty, team management, and back of house operations.

The business generates revenue through three segments:

Subscription Services: SaaS fees charged per location, based on the number of software products, configuration, and employee headcount.

Financial Technology Solutions: Transaction based revenue from payment processing facilitated through the platform.

Hardware & Professional Services: Revenue from the sale of handheld devices, tablets, terminals, and accessories, along with installation and training fees.

(Source: Toast Investor Relations Presentation)

Investment Thesis:

We believe Toast is a high quality business trading at a discounted valuation that the market does not fully understand.

Toast has built the operating system for the restaurant industry. Through a single, unified platform, restaurants manage their entire workflow, from menu configuration and order taking, to kitchen coordination, payment processing, and payroll. Rather than stitching together a patchwork of vendors, Toast customers get one product that runs the business end to end. That depth of integration creates real switching costs and makes Toast genuinely sticky.

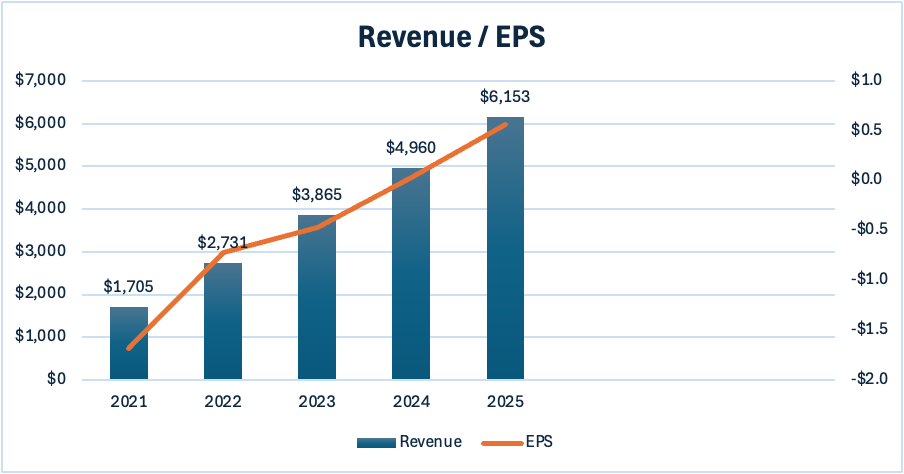

The operating results reflect this position. In fiscal year 2025, Toast added 30,000 net new locations, grew Gross Payment Volume (GPV) 23%, expanded Annual Recurring Revenue (ARR) 26%, and delivered Recurring Gross Profit growth of 33%. This is not a company in survival mode, it is a business compounding at scale while the market is distracted by AI narratives.

Why does the opportunity exist? Two reasons. First, the broader AI driven selloff in SaaS has unjustifiably punished Toast alongside lower quality peers, even though the case for AI meaningfully disrupting restaurant operations software in the near term is far from clear.

Second, competitive concerns around players like Shift4 and Square have weighed on sentiment. But the market is missing something, Toast is solely focused on restaurants. While competitors spread their attention across retail, e-commerce, and enterprise payments, Toast has spent years going deep on the specific, complex needs of the restaurant industry.

Valuation:

Given Toast’s high growth rate, we assessed valuation primarily through revenue based multiples rather than static earnings metrics.

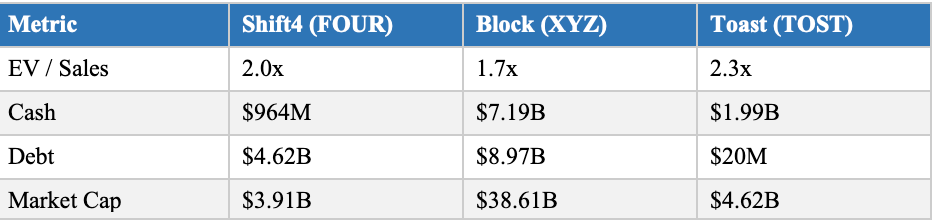

Toast currently trades at an EV/Revenue multiple of 2.3x, meaning for every $1 of revenue, the market is paying $2.30. On the surface, that is a modest premium for a business growing at this pace.

On an EV/EBITDA basis, Toast trades at approximately 38x. Without context, that sounds elevated. But when you layer in the trajectory of the business, the picture changes significantly. Toast has been adding approximately $1.2 billion in revenue per year since fiscal year 2023. More importantly, EBITDA margins have expanded from -6.0% in 2023 to +6.7% in 2025, a 1,270 basis point improvement in just two years. Revenue is scaling faster than costs, and the business is inflecting.

Toast has also been able to compound revenue by roughly 38% annually since the IPO, while EPS turned positive for the first time in 2024 and continued to accelerate in 2025.

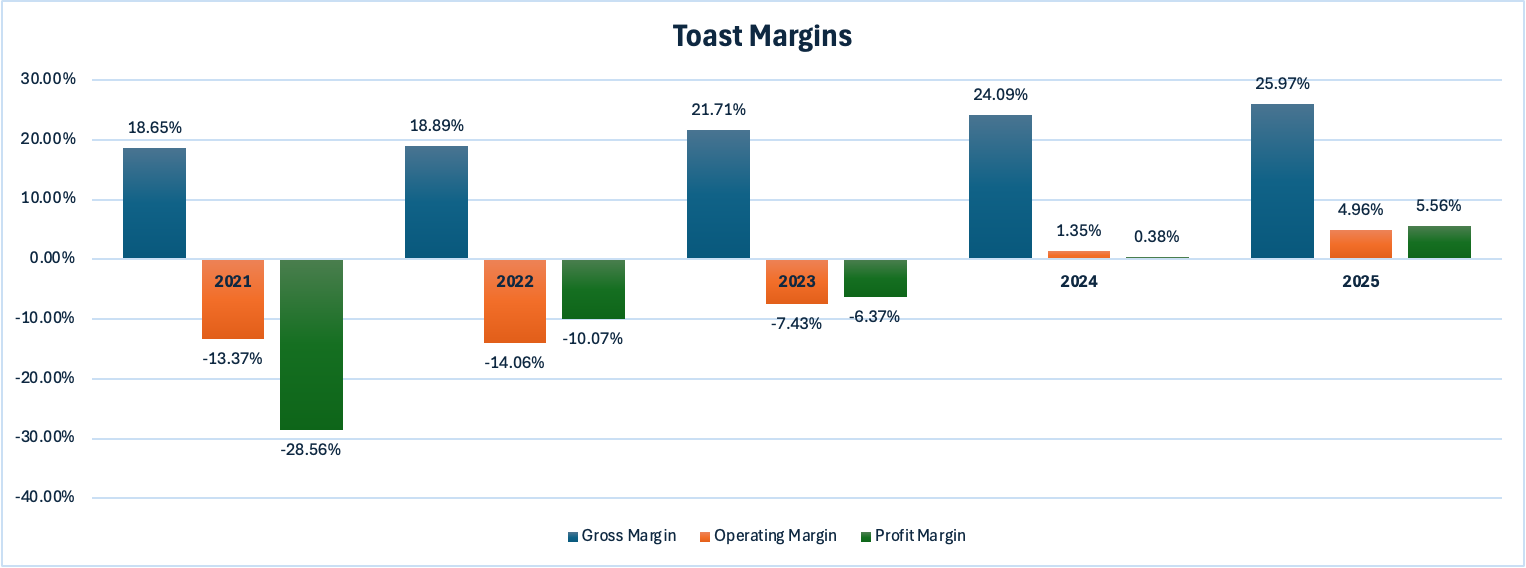

Since going public, Toast has demonstrated five years of consistent margin expansion, with operating and profit margins now positive and accelerating.

Put all together, we believe the market is undervaluing the pace and durability of Toast’s margin expansion. The EV/EBITDA multiple looks high by itself, but if you factor in the margin growth, it is more than justified.

For context, here is how Toast compares to its closest publicly traded peers:

One additional point worth highlighting, unlike many of its payment processing peers, Toast does not rely on M&A for growth. Its location count, GPV, and ARR expansions are all organic. This is a meaningful quality differentiator that we believe the market also underappreciates.

Risks:

With any investment comes risk.

The first is the SaaS selloff. Toast has been caught in the sell off of software stocks driven by AI sentiment. We believe this is largely unrelated to Toast’s business and represents an opportunity, but the overhang on the stock is real in the near term.

The second and most important structural risk is that Toast’s singular focus on restaurants is both its greatest strength and its greatest source of concentration risk. Restaurants operate on thin margins and are sensitive to labor costs, inflation, and consumer sentiment. Toast’s growth story depends in part on new restaurant locations opening and existing locations remaining viable. The U.S. restaurant industry has a roughly 10% annual failure rate even during favorable economic conditions, and a meaningful deterioration in the macro environment could pressure Toast’s net location growth.

The third risk is regulatory. Toast currently earns an attractive payment processing margin of approximately 55 basis points. Regulators have become increasingly critical of surcharging practices in the payments industry, and any adverse regulatory action targeting processing fees could pressure this revenue stream.

Recent Catalysts:

Over the past several months, Toast has announced product and partnership developments that reinforce the long term thesis.

Toast IQ

Toast’s new AI powered operations layer, Toast IQ, automates inventory management, menu optimization, and pricing recommendations. Rather than relying on manual analysis, restaurants can now access data driven suggestions grounded in their own business trends and local market conditions.

New Enterprise Partnerships

Toast has secured three significant new partnerships that validate its enterprise level capabilities:

Applebee’s

Uber

Coca-Cola

These partnerships signal that Toast is beginning to win at scale with national brands, a market segment that adds significant ARR per location and carries strong retention characteristics.

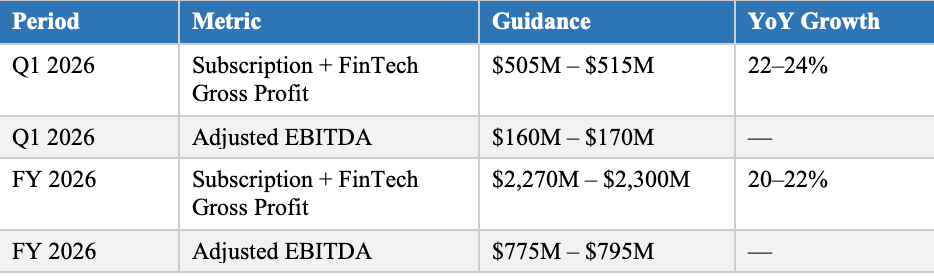

Fiscal Year 2026 Guidance:

Management has issued the following guidance for fiscal year 2026:

Management’s guidance implies continued double digit gross profit growth and a significant step up in EBITDA, consistent with our operating leverage thesis.

Summary:

Toast has built a genuinely differentiated business in a large and underserved market. The platform is deeply embedded in its customers operations, the growth trajectory is strong, and the margin expansion story is playing out ahead of expectations. The current valuation does not reflect the durability of Toast’s competitive position or the earnings power developing beneath the surface.

We added Toast to our portfolio and believe it will continue to compound as the market comes to appreciate what this business has built.

Disclaimer

Atlas Capital Research is not investment advice.

As a reader of Atlas Capital Research, you agree with our disclaimer. Please read the full disclaimer here.